Diarmuid McDonnell & Alasdair Rutherford, 2017

As Corrado “Junior” Soprano, plagiarising a Chinese curse of dubious provenance, puts it: may you live in interesting times. Charities in the UK have been the subject of intense media, political and public scrutiny in recent years, resulting in three parliamentary inquiries. Public confidence and trust in the sector has been questioned in light of various “scandals” including unethical fundraising practices (resulting in the establishment of a new fundraising regulator for England and Wales in 2016), high levels of chief executive pay, politically-motivated lobbying and advocacy work, and poor financial management. Using novel data supplied by the Office of the Scottish Charity Regulator (OSCR), my colleague Dr Alasdair Rutherford and I describe the nature and extent of alleged and actual misconduct by Scottish charities, and ask what organizational and financial factors are associated with this outcome?

Background

First, some background on what we mean when we say “charity”. The Scottish Charity Register is maintained by OSCR which was established in 2003 as an Executive Agency and took up its full powers when the Charities and Trustee Investment (Scotland) Act 2005 came into force in April 2006. In Scotland, a charity is defined (under statute) as an organization that is listed on the Register after demonstrating that it passes the charity test: it must have only charitable purposes; the organization must or intend to provide some form of public benefit; it must not allow its assets to be used for non-charitable purposes; it cannot be governed or directed by government ministers; and it cannot be a political party. One of OSCR’s main responsibilities is to identify and investigate apparent misconduct and protect charity assets. It operationalises this duty by opening an investigation (what they term an inquiry) into the actions of a charity suspected of misconduct and other misdemeanours.

Investigations are mainly initiated as a result of a public complaint but they can also be opened by a referral from a department in OSCR or another regulator. For example, one of the founders of the charity The Kiltwalk reported the organization to OSCR on the grounds that he has concerns over the amount of funds raised by the organization that are spent on meeting the needs of beneficiaries. OSCR can only deal with concerns that relate to charity law – such as damage to charitable assets or beneficiaries, misconduct or misrepresentation – though it can refer cases to other bodies such as when criminal activity is suspected. Finally, the outcome is recorded for each investigation. Outcomes are varied and often specific to each investigation but most can be related to three common categories: no action taken or necessary; advice given; and regulatory intervention.

Method

This study examines two dimensions of charity misconduct that deserve greater attention: regulatory investigation and subsequent action. Regulatory action can take the following two, broad forms: the provision of advice (e.g. recommending a charity improve its financial controls to counteract the threat of fraud or misappropriation) and the use of OSCR’s formal regulatory powers (e.g. reporting the charity to prosecutors or suspending trustees). This study overcomes many of the limitations outlined previously by utilising a novel administrative dataset, derived from OSCR, covering the complete population (current and historical) of registered Scottish charities. It is constructed from three sources: the Scottish Charity Register, which is the official, public record of all charities that have operated in Scotland; annual returns, which are used to populate many of the fields on the Register (e.g. annual gross income); and internal OSCR departmental data relating to misconduct investigations. Once linked using each observation’s Scottish Charity Number, this dataset contains 25,611 observations over the period 2006-2014.

The outcome of being investigated by the regulator is measured using a dichotomous variable that has the value 1 if a charity has been investigated and 0 if not. The other two dependent variables are also dichotomous: regulatory action takes the value 1 if a charity has had regulatory action taken against it and 0 if not; and intervention takes the value 1 if a charity is subject to regulatory intervention and 0 if not (i.e. it received advice instead). The dependent variables are modelled using binary logistic regression. We model the probability of investigation using binary logistic regression as a function of organization size, age, institutional form, field of operations and geographical base. For the sub-sample of organizations that were investigated, we then model the probability of regulatory action, and its different forms, being taken based on the same characteristics plus the source of the complaint made.

Describing Investigations and Regulatory Action

There have been 2,109 regulatory investigations of 1,566 Scottish charities over the study period: this represents six percent of the total number of organizations active during this time. The number of investigations increased steadily during OSCR’s early years and then plateaued at around 400 per year until 2013/14, when the figure declined slightly. The majority of investigations (78 percent) concerned charities that were investigated only once in their history. A little over 30 percent of investigations resulted in regulatory action being taken against a charity: 16 percent received advice and 13 percent experienced intervention by OSCR.

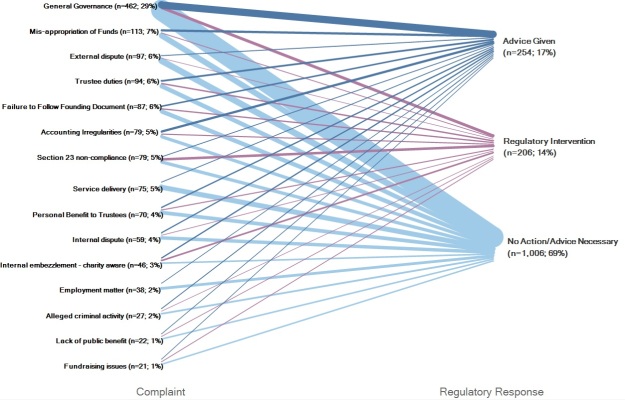

It is a member of the public that is most likely to contact OSCR with a concern about a charity. Internal stakeholders of the charity account for 31 percent of all investigation initiators, though this disregards the strong possibility that many of those recorded as anonymous are involved in the running of the charity they have a concern about. The concerns that prompt these actors to raise a complaint with OSCR are numerous and diverse. Figure 1 below visualizes the associations between the most common types of complaint and the response of the regulator. The overriding concern is general governance, as well as associated issues such as the duties of trustees and adherence to the founding document. Financial misconduct also ranks highly, particularly the misappropriation of funds and suspicion of financial irregularity.

Figure 1. Association between type of complaint and regulator response

Note: Each complaint can have two types, and maps to one of the regulatory responses. The fifteen most common complaint types are shown. The thickness of the line is proportional to the number of complaints leading to each regulatory response.

Modelling the Risk of Investigation and Action

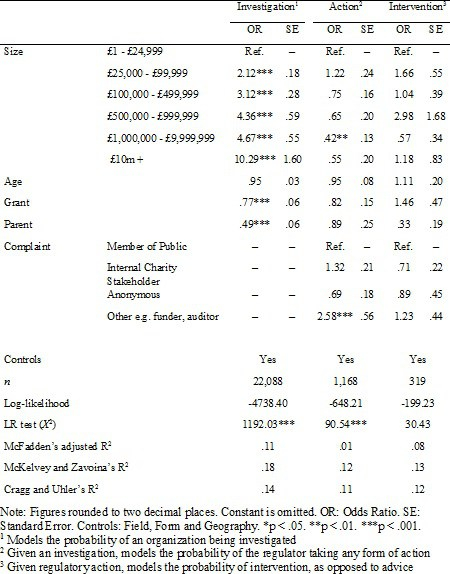

In Table 3, we report the odds ratios (exponentiated coefficients) rather than the log odds as they approximate the relative risk of each outcome occurring. This is appropriate not only for ease of interpretation but because the absolute chance of either outcome occurring is low (i.e. it is better to know which charities are more likely relative to their peers). The category with the most observations is chosen as the base category for each nominal independent variable.

Table 1. Results of Logistic Regression on dependent variables

We first examine the effects of organization age and size on the outcomes. The coefficient for age varies across the three outcomes. A one-unit increase in the log of age results in a five percent decrease in the odds of being investigated or being subject to regulatory action; however, the odds of experiencing intervention compared to receiving advice are higher for older charities. There appears to be a clear income gradient present in the investigation model: as organization size increases so do the odds of being investigated compared to the reference category. With regards to the actor that initiates an investigation, it appears that stakeholders with a monitoring role (e.g. funders, auditors or other regulators) are more likely than members of the public to report concerns that warrant some form of regulatory action; in contrast, internal charity stakeholders such as employees and volunteers have higher odds of identifying concerns that merit the provision of advice by OSCR and lower odds of triggering regulatory intervention in their charity. While size predicts complaints, it is the source of the complaint that is a more reliable predictor of the need for regulators to take action.

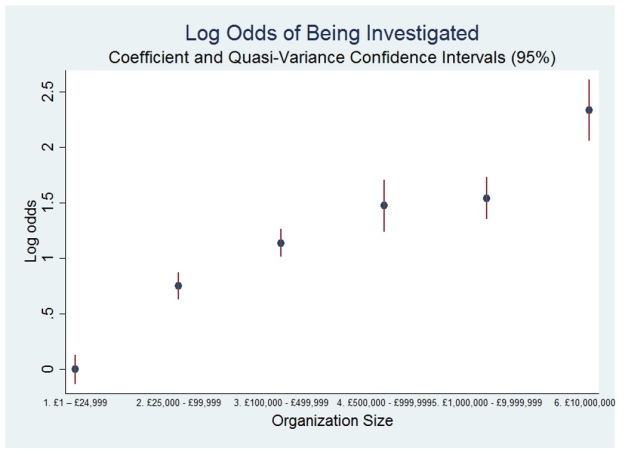

A more nuanced examination of the effect of organization size is possible by comparing categories of this variable to each other and not just the base category (shown in Figure 2). Drawing on suggestions by Firth (2003), Firth and Menezes (2004), and Gayle and Lambert (2007), we employ quasi-variance standard errors to ascertain whether categories of organization size are significantly different from each other. Unsurprisingly, the largest charities have significantly higher odds than all other categories; however it appears that the middle categories (charities with income between £100,000 and £1m) are not significantly different from each other and neither are organizations between £500,000 and £10m.

Figure 2. Quasi-Variance log odds of being investigated

Conclusion

The results of the multivariate analysis point to the factors associated with charity investigation and misconduct, showing the mismatch between those predicting complaints and those predicting regulatory action. This has considerable implications for charity regulators seeking to deploy their limited resources effectively and in a way that ultimately protects and enhances public confidence. By revealing the disconnect between the level of complaints and concerns that require regulatory action, we argue there is much work to do for practitioners in the sector with regards to charity reputation and stakeholder communication. Charity boards are ultimately responsible for the governance of their organization, and must ensure that adequate policies and procedures are in place. This includes reducing the risk of misconduct occurring, taking corrective action in response to guidance from the regulator, and developing the management and reporting functions required to deal with the consequences. Recognition should also be given to the role that stakeholders such as funders and auditors must play in self-regulation of the sector, given their proximity to charities through their day-to-day activities. It is no longer sufficient (if indeed it ever was) to rely on charity status to convey trust and inspire confidence in the conduct of an organization.